Most of us have life and financial goals that are intertwined. Whether that means buying a home, launching a nonprofit by age 30, having three kids and putting them through college, or all of the above, reaching those aspirations takes planning and focus.

Solid financial planning can help you realize those dreams. Here’s your guide to setting smart money goals and achieving them, step by simple step.

Check out our Money Management Guide.

This article is from SoFi’s guide on how to manage your money, where you can learn basic money management tips and strategies.

Key Points

• Identify and prioritize financial goals, including both short-term and long-term objectives.

• Apply S.M.A.R.T. criteria to set specific, measurable, achievable, relevant, and time-bound goals.

• Track spending meticulously to manage and adhere to a budget effectively.

• Focus on paying off high-interest debt to enhance overall financial health.

• Regularly review and adjust financial goals to align with changing personal circumstances.

What Are Financial Goals?

Financial goals are the aspirations you have for how you will bring in income, spend it, and save it. These can be short-term dreams, like financing a vacation to Tulum next winter, or longer-term ones, such as retiring by age 50.

Identifying these goals and then creating a roadmap to achieve them is what smart financial management typically boils down to.

Short-Term Financial Goals

Short-term goals are usually defined as things you want to achieve with your personal finances typically within a year.

Examples of short-term financial goals could be anything from starting an emergency fund to finding a budget that works for you to saving up for a new mobile phone.

Long-Term Financial Goals

When you pull back and think big-picture about money management, you have likely entered the realm of long-term financial goal setting. These are goals that can take several years or even decades to achieve.

Examples of long-term goals would be saving enough money to buy a house, putting your kids through college, or retiring comfortably.

What Are S.M.A.R.T. Goals?

When you are thinking about your financial goals and doing some research, you may come upon the acronym S.M.A.R.T. Think of this as a guideline to help you set and achieve your money aspirations. Here’s what it stands for:

• S for Specific: Instead of your goal being “to be financially comfortable,” try to be more precise. Perhaps your goal would be to have no debt except your mortgage and a certain amount in your retirement fund.

• M for Measurable: It can be wise to assign real numbers to your goals. For instance, to save $200K in your kids’ college funds is a measurable aspiration. Just saying, “to pay for college” can be too vague to work toward.

• A for Achievable: Setting unrealistic expectations can lead to frustration and disappointment. Think about your lifestyle, income potential, cost of living, and other key factors, and set reasonable goals.

• R for Realistic: Similarly, plan steps to achieve your goals realistically. Don’t expect to cut your expenses to the rock bottom or ignore the impact of inflation over time.

• T for Time-based: Give yourself specific goals and due dates, such as “Save $500 a month until I have $5,000 in my emergency fund 10 months from now.”

How to Set Financial Goals

Next, consider the specific steps of setting financial goals. Break it down as follows:

1. Assessing Your Finances

Figuring out exactly what your current finances look like is a vital step. Sure, you probably know when you get paid, but have you checked how much is going toward your retirement savings fund every pay period or — gulp — exactly how much you’re spending on food delivery? Keeping a close eye on your finances might help you set smarter money goals.

It might seem easy to ignore the finer details of our finances in favor of blissful ignorance, but failing to know where you and your money stand might harm your financial health down the line.

So if you haven’t looked at where your money is going in a while, taking a look at how much money you’re bringing in, how much you’re spending, and how much you’re saving might help you set more meaningful money goals.

• Check out your bank statements, credit card statements, and even online banking records to help you determine where your money is going every month.

• Write down big numbers like credit card, personal loan, or student loan debt. This can help you plan for payoff.

• Consider using tech tools to help you wrangle your finances. There are plenty of apps you can download, and online banking might be able to help you too. Typically, banks offer apps where users can easily access details about their spending and balances. Your credit card bill or app can also often provide a graphic representation of where your dollars fly off to each month.

2. Figuring Out What Is Most Important to You

Once you have a snapshot of your overall financial situation, it can be worthwhile to spend some time reflecting on your money goals: what is really important to you.

While there are many things a person ideally should be saving for, like a down payment on a house or retirement fund, your financial goals might not be the same as your sibling’s or your coworker’s.

Just like your parents always told you: You’re unique. And so is the process of setting financial goals. What might they look like?

• You might want to pay off student debt as fast as possible in order to free up more cash every month.

• You might be working toward public service loan forgiveness and not be as focused on quickly paying off student loans.

• Perhaps your financial goal is to save up an emergency fund or take a vacation in six months.

• You might want to retire and move to another country by the time you’re 55.

It’s likely that your goals will be a mix of short-term and long-term aspirations, as described above.

Increase your savings

with a limited-time APY boost.*

3. Establishing a Fun Budget

Okay, but what if you just want to go clothes shopping once a month without feeling guilty or take that Budapest vacation you’ve been dreaming about?

Make it work! Setting a financial goal is all about having your money serve you. Here are some pointers:

• Planning out your discretionary spending might not only help keep your finances on track but can also help you inject an extra fun quotient into your life. That’s a win-win.

• When a budget is too harsh and punitive, you might wind up making impulse buys or otherwise overspending. If you know you have some cash stashed for mood-lifting purposes, you can hopefully avoid that scenario.

But whether you’re focused on saving up for a down payment on a house or a trip to Disneyland, you won’t get there without a plan. Making a budget will get you focused and help you take control of your finances.

4. Staying On Track

Once you’ve decided on a money goal or two, it’s time to put a plan into action. Your plan will vary depending on whether you’re tackling a long-haul climb out of credit card debt or saving an emergency fund. A bit of advice:

• Managing your money isn’t a “set it and forget it” proposition. Life happens. You may get a raise one month, and then have a (surprise!) major dental bill the next. It’s important to check in with your money regularly.

• Adapt your budget when things shift. Everything from getting a nice bonus to having a baby can be a good reason to check in with your money goals and recalibrate.

• Whatever your financial goals, there are tools that can help you along on your financial journey. Having the right banking partner can play a crucial role. Look for a bank that can help you set up automatic deductions from your checking account on payday to savings toward your financial goals. And find a bank that doesn’t charge you all kinds of fees; after all, they’re enjoying the privilege of using the money you’ve deposited!

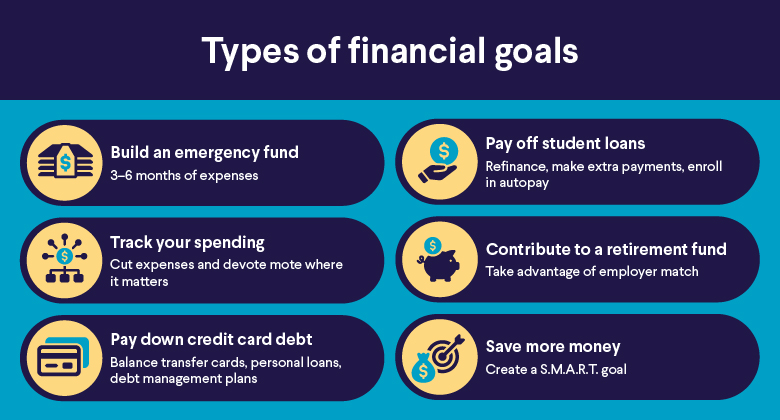

6 Examples of Financial Goals to Consider

If you’re looking for help brainstorming how to manage your money aims, here are some popular financial goal examples to consider:

1. Build an Emergency Fund

Whether you’re easily covering your monthly expenses or grabbing change from the bottom of your bag to buy a coffee, many people are living paycheck to paycheck. But what if that paycheck disappeared or if you had a large, unexpected expense? Enter the emergency fund.

Recent history has taught us a lot about how emergencies can arise. Stashing away an emergency fund might help you comfortably weather a pandemic, a “company-wide restructuring” that eliminates your position, or an unexpected illness that cuts into your freelance earnings.

Consider a long-term financial goal of setting aside about three to six months’ worth of expenses. Use an online emergency fund calculator to do the math and help you save at the right rate.

2. Track Your Spending

As mentioned above, keeping track of your expenses is important. Sometimes, spending that starts as an occasional thing (that TGIF latte) becomes a regular expense that drags down your budget.

Or you might find that you are dealing with lifestyle creep, which occurs when you earn more but your spending rises too, keeping you at the same level of wealth.

If you track your expenses, you can see how your money is tracking. You might decide to cut back on streaming services or realize that now that you’ve paid off your credit card debt, you could put more toward retirement.

3. Pay Down Credit Card Debt

High-interest credit card debt can feel like a treadmill: You keep putting in more and more effort, seemingly without getting closer to the finish line. Many people carry credit card debt, which can cut into your ability to save. What’s more, if your balance is more than 30% of your card’s credit limit, your credit-utilization ratio may negatively impact your credit score. In fact, it’s ideal to use only 10% or less of your credit limit.

It’s no wonder that for many of us, setting a financial goal involves the words “pay off my credit card.” Indeed, making a plan to pay down debt instead of focusing on those minimum monthly payments could help you dramatically improve your finances. Your credit card statement will tell you how much to pay to get rid of debt in three years; that can be a helpful guideline.

If you need other options, consider:

• A balance-transfer credit card, which offers low or no interest for a period of time (typically 6 to 18 months), may also be useful.

• A personal loan, which may offer a lower interest rate. You can use that to pay off the credit card debt and then have a lower amount due to pay off the loan.

• You might also consider a debt management plan or meeting with a nonprofit debt counseling agency if you feel you need additional help.

When you get out from under the burden of this kind of debt, other doors (like to a home you own) may open. It can give your budget just the kind of breathing room you crave.

4. Pay Off Student Loans

Paying off student loans is another move that can help you reach your financial goals. Doing so frees up funds in your budget for other uses. Some ideas:

• Make extra payments toward the principal when possible. That might mean a little more every month or applying a windfall like a tax refund.

• Refinance a student loan. This could potentially lower your rate and help you pay off your debt sooner.

• Pay biweekly instead of monthly. This means you make an extra payment each year, again helping shorten the timeline to becoming free of student loan debt.

• Enroll in autopay. Federal student loan servicers and many private lenders will lower your interest rate a bit if you opt into automatic payments. While it won’t make a huge dent in what you owe, every little bit can help.

5. Contribute to Your Retirement Fund

Most of us know we should be saving for retirement, but that financial goal can be easier said than done when there are so many competing places to put our money.

The good news is that when you set up a retirement account and start saving, even small amounts can grow over time, which makes saving for your golden years a great financial goal. Contributing regularly — whether through your employer’s plan or an IRA — is worthwhile, especially when inflation is high.

Many experts say that a smart financial goal is to be saving 10% to 15% of your pre-tax paycheck for your retirement. One smart move: If your employer offers a company match of dollars put toward retirement, put in at least the minimum required to snag it. So if your company says you must contribute 6% of your salary to get a 50% match, that means if you put in 6%, they will add 3% to your savings. Don’t leave that money on the table!

6. Save More Money

Another way to hit your financial goals, big and small, is to save more money. Here are a few techniques:

• Automate your savings. Set up seamless recurring deductions from checking to savings for just after payday. Doing so means you don’t have to remember to allocate the funds. And you won’t see the money sitting in checking, tempting you to go shopping with it.

• Challenge yourself each month to give up an expense. For instance, don’t buy any pricey coffees for one month and put aside the savings. Next month, no movies. The following, no takeout lunches. You can do it!

• See about bundling insurance premiums or paying annually vs. monthly to save money.

• Negotiate bills. See if your credit card provider will lower your rate, for starters.

Recommended: Passive Income Ideas

How to Adjust Your Financial Goals if Your Circumstances Change

Sometimes, life throws you curveballs. You don’t get the raise you were hoping for. A family member has a medical issue that requires more money to manage than you expected. Or you move to a new town with a higher cost of living.

In these situations, you may need to ramp down some of your financial goals. Perhaps you can’t have that emergency fund fully saved by the end of this year. You could lower how much you put away and reconcile yourself to the fact that you won’t meet your goal as soon as you would have liked.

This is just another reason why checking in with your money and adjusting your budget often is important.

And don’t forget the bright side: If you get a major salary bump or a windfall, you can use that to crush your goals that much sooner. Staying flexible can be vital, regardless of which way your finances are trending.

The Takeaway

Setting smart financial goals is an important step in managing your money and achieving your life goals.

By taking such steps as evaluating your financial situation, creating a budget, and setting smart benchmarks, you can be on track to check off your aspirations. Whether that means saving for summer vacations, eliminating credit card debt, or retiring early, taking control of your money can be a very good feeling. And finding the right banking partner can help make the process even easier.

Interested in opening an online bank account? When you sign up for a SoFi Checking and Savings account with direct deposit, you’ll get a competitive annual percentage yield (APY), pay zero account fees, and enjoy an array of rewards, such as access to the Allpoint Network of 55,000+ fee-free ATMs globally. Qualifying accounts can even access their paycheck up to two days early.

FAQ

What is a good financial goal?

Financial goals need to reflect what’s important to you, but for most people, they are a mix of short-term aspirations (like having an emergency fund and minimizing credit-card debt) and long-term plans, like retirement savings.

How do you stick to a financial goal?

Sticking to a financial goal can be easier if you set up automatic deductions that transfer money from checking (where you might be tempted to spend it) to savings. Also, getting familiar with your finances, developing a plan, and regularly checking your progress are good moves.

What are some money management tips?

It’s a good idea to assess your finances and make short- and long-term goals. Then, allocate a percent of your earnings and set up automatic deductions to your savings; pay down high-interest debt (like credit cards); establish an emergency fund; and start saving for retirement. Even if it’s just a small amount, it will grow!

SoFi® Checking and Savings is offered through SoFi Bank, N.A. ©2025 SoFi Bank, N.A. All rights reserved. Member FDIC. Equal Housing Lender.

The SoFi Bank Debit Mastercard® is issued by SoFi Bank, N.A., pursuant to license by Mastercard International Incorporated and can be used everywhere Mastercard is accepted. Mastercard is a registered trademark, and the circles design is a trademark of Mastercard International Incorporated.

SoFi members with Eligible Direct Deposit activity can earn 3.80% annual percentage yield (APY) on savings balances (including Vaults) and 0.50% APY on checking balances. Eligible Direct Deposit means a recurring deposit of regular income to an account holder’s SoFi Checking or Savings account, including payroll, pension, or government benefit payments (e.g., Social Security), made by the account holder’s employer, payroll or benefits provider or government agency (“Eligible Direct Deposit”) via the Automated Clearing House (“ACH”) Network during a 30-day Evaluation Period (as defined below).

Although we do our best to recognize all Eligible Direct Deposits, a small number of employers, payroll providers, benefits providers, or government agencies do not designate payments as direct deposit. To ensure you're earning 3.80% APY, we encourage you to check your APY Details page the day after your Eligible Direct Deposit arrives. If your APY is not showing as 3.80%, contact us at 855-456-7634 with the details of your Eligible Direct Deposit. As long as SoFi Bank can validate those details, you will start earning 3.80% APY from the date you contact SoFi for the rest of the current 30-day Evaluation Period. You will also be eligible for 3.80% APY on future Eligible Direct Deposits, as long as SoFi Bank can validate them.

Deposits that are not from an employer, payroll, or benefits provider or government agency, including but not limited to check deposits, peer-to-peer transfers (e.g., transfers from PayPal, Venmo, etc.), merchant transactions (e.g., transactions from PayPal, Stripe, Square, etc.), and bank ACH funds transfers and wire transfers from external accounts, or are non-recurring in nature (e.g., IRS tax refunds), do not constitute Eligible Direct Deposit activity. There is no minimum Eligible Direct Deposit amount required to qualify for the stated interest rate. SoFi members with Eligible Direct Deposit are eligible for other SoFi Plus benefits.

As an alternative to Direct Deposit, SoFi members with Qualifying Deposits can earn 3.80% APY on savings balances (including Vaults) and 0.50% APY on checking balances. Qualifying Deposits means one or more deposits that, in the aggregate, are equal to or greater than $5,000 to an account holder’s SoFi Checking and Savings account (“Qualifying Deposits”) during a 30-day Evaluation Period (as defined below). Qualifying Deposits only include those deposits from the following eligible sources: (i) ACH transfers, (ii) inbound wire transfers, (iii) peer-to-peer transfers (i.e., external transfers from PayPal, Venmo, etc. and internal peer-to-peer transfers from a SoFi account belonging to another account holder), (iv) check deposits, (v) instant funding to your SoFi Bank Debit Card, (vi) push payments to your SoFi Bank Debit Card, and (vii) cash deposits. Qualifying Deposits do not include: (i) transfers between an account holder’s Checking account, Savings account, and/or Vaults; (ii) interest payments; (iii) bonuses issued by SoFi Bank or its affiliates; or (iv) credits, reversals, and refunds from SoFi Bank, N.A. (“SoFi Bank”) or from a merchant. SoFi members with Qualifying Deposits are not eligible for other SoFi Plus benefits.

SoFi Bank shall, in its sole discretion, assess each account holder’s Eligible Direct Deposit activity and Qualifying Deposits throughout each 30-Day Evaluation Period to determine the applicability of rates and may request additional documentation for verification of eligibility. The 30-Day Evaluation Period refers to the “Start Date” and “End Date” set forth on the APY Details page of your account, which comprises a period of 30 calendar days (the “30-Day Evaluation Period”). You can access the APY Details page at any time by logging into your SoFi account on the SoFi mobile app or SoFi website and selecting either (i) Banking > Savings > Current APY or (ii) Banking > Checking > Current APY. Upon receiving an Eligible Direct Deposit or receipt of $5,000 in Qualifying Deposits to your account, you will begin earning 3.80% APY on savings balances (including Vaults) and 0.50% on checking balances on or before the following calendar day. You will continue to earn these APYs for (i) the remainder of the current 30-Day Evaluation Period and through the end of the subsequent 30-Day Evaluation Period and (ii) any following 30-day Evaluation Periods during which SoFi Bank determines you to have Eligible Direct Deposit activity or $5,000 in Qualifying Deposits without interruption.

SoFi Bank reserves the right to grant a grace period to account holders following a change in Eligible Direct Deposit activity or Qualifying Deposits activity before adjusting rates. If SoFi Bank grants you a grace period, the dates for such grace period will be reflected on the APY Details page of your account. If SoFi Bank determines that you did not have Eligible Direct Deposit activity or $5,000 in Qualifying Deposits during the current 30-day Evaluation Period and, if applicable, the grace period, then you will begin earning the rates earned by account holders without either Eligible Direct Deposit or Qualifying Deposits until SoFi Bank recognizes Eligible Direct Deposit activity or receives $5,000 in Qualifying Deposits in a subsequent 30-Day Evaluation Period. For the avoidance of doubt, an account holder with both Eligible Direct Deposit activity and Qualifying Deposits will earn the rates earned by account holders with Eligible Direct Deposit.

Separately, SoFi members who enroll in SoFi Plus by paying the SoFi Plus Subscription Fee every 30 days can also earn 3.80% APY on savings balances (including Vaults) and 0.50% APY on checking balances. For additional details, see the SoFi Plus Terms and Conditions at https://www.sofi.com/terms-of-use/#plus.

Members without either Eligible Direct Deposit activity or Qualifying Deposits, as determined by SoFi Bank, during a 30-Day Evaluation Period and, if applicable, the grace period, or who do not enroll in SoFi Plus by paying the SoFi Plus Subscription Fee every 30 days, will earn 1.00% APY on savings balances (including Vaults) and 0.50% APY on checking balances.

Interest rates are variable and subject to change at any time. These rates are current as of 1/24/25. There is no minimum balance requirement. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet.

*Awards or rankings from NerdWallet are not indicative of future success or results. This award and its ratings are independently determined and awarded by their respective publications.

SoFi Loan Products

SoFi loans are originated by SoFi Bank, N.A., NMLS #696891 (Member FDIC). For additional product-specific legal and licensing information, see SoFi.com/legal. Equal Housing Lender.

Disclaimer: Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website .

SoFi Private Student Loans

Please borrow responsibly. SoFi Private Student loans are not a substitute for federal loans, grants, and work-study programs. We encourage you to evaluate all your federal student aid options before you consider any private loans, including ours. Read our FAQs.

Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. SoFi Private Student loans are subject to program terms and restrictions, such as completion of a loan application and self-certification form, verification of application information, the student's at least half-time enrollment in a degree program at a SoFi-participating school, and, if applicable, a co-signer. In addition, borrowers must be U.S. citizens or other eligible status, be residing in the U.S., Puerto Rico, U.S. Virgin Islands, or American Samoa, and must meet SoFi’s underwriting requirements, including verification of sufficient income to support your ability to repay. Minimum loan amount is $1,000. See SoFi.com/eligibility for more information. Lowest rates reserved for the most creditworthy borrowers. SoFi reserves the right to modify eligibility criteria at any time. This information is subject to change. This information is current as of 4/22/2025 and is subject to change. SoFi Private Student loans are originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org).

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Third Party Trademarks: Certified Financial Planner Board of Standards Center for Financial Planning, Inc. owns and licenses the certification marks CFP®, CERTIFIED FINANCIAL PLANNER®

SOBNK-Q325-027